Homebuyers is struggling with increasing down costs

New Government Homes Fund Agency’s (FHFA) brand new conforming financing limits to own 2024 indicate homeowners is now able to score big mortgage loans backed by Fannie mae and you can Freddie Mac computer.

The newest financial restrict to have old-fashioned finance supported by Fannie and Freddie is $766,550, a rise regarding $forty,350 out-of 2023. Into the highest-pricing places that 115% of the regional average domestic well worth try bigger than $766,550, homeowners could be permitted to make use of the higher-pricing city financing limitation, which is 150% off normal loan limits. You to definitely pushes the fresh restrict for high-pricing elements so you’re able to $1,149,825.

The option follows the fresh new rapid obtain in home pricing over the U.S., although home loan cost improved. Home prices rose 5.5% amongst the third one-fourth off 2022 as well as the 3rd one-fourth regarding 2023 and you may were right up dos.1% compared to 2nd quarter regarding 2023, according to FHFA House Rate Index.

“The newest mortgage constraints essentially indicate that property owners who have seen rates appreciate can refi on the a good Fannie otherwise Freddie mortgage,” Charles Williams, founder and Ceo off real estate and you may home loan behavioural investigation seller Percy. “Basically, with the limit elevated so you can $766,550 of $726,2 hundred, the FHFA is actually staying its lending assistance in lockstep which have household rate appreciate. The same goes towards FHA. This is exactly great but also for potential real estate buyers who would like to pick within high end of the the fresh new maximum.”

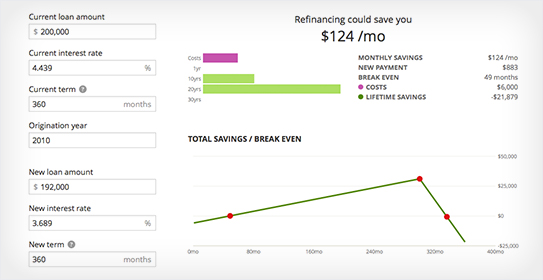

For many who currently have an excellent jumbo financing that you like so you’re able to transfer to a traditional home mortgage, otherwise your house speed possess enjoyed that’s today shielded lower than this new constraints, you could consider refinancing to save on your own payment per month. You can visit Reputable to compare several lenders at the same time and choose the one that is the greatest complement your.

FHA introduces limits, too

The brand new Government Housing Administration (FHA) revealed limitations to possess 2024 because of its Unmarried Family Name II send and Domestic Equity Sales Financial (HECM) insurance coverage software. Loan limits to own FHA submit mortgage loans often increase in step 3,138 counties and will will always be unchanged in 96 areas on the year ahead on account of domestic rates enjoy inside the very first 50 % of out-of 2022.

FHA finance is actually covered of the Service out-of Houses and you may Urban Innovation (HUD). FHA funds offer off money as low as 3.5%, credit ratings as low as 580, and you will a flexible financial obligation-to-earnings proportion, permitting alot more home buyers be considered, specifically earliest-day homebuyers.

“The statutory financing limit increases revealed now mirror the brand new proceeded go up in home cost viewed while in the all the nation for the 2023,” Secretary Assistant to have Construction and you will Federal Casing Administrator Julia Gordon told you. “The brand new expands so you can FHA’s mortgage restrictions tend to allow homeowners to use FHA’s reduced-down-commission capital to gain access to homeownership immediately when a shortage off cost threatens to close well-qualified consumers out of the business.”

The new Federal Housing Work (NHA) requires the FHA to put solitary-relatives give home mortgage constraints based on a formula that uses state or Urban Statistical City (MSA) home business analysis so you’re able to derive the latest financing constraints into three various other rates classes created by laws.

The new FHA based their floor and ceiling loan constraints centered on this new federal conforming loan limitation put by FHFA ($766,550). FHA’s 2024 lowest federal financing maximum flooring of $498,357 getting a-one-unit house is 65% of one’s federal conforming loan maximum.

One city where the loan limit exceeds that it floor is recognized as a great “high-pricing city.” During the higher-prices section, the fresh FHA kits differing financing constraints above the floors considering the fresh new median home rate in for each area. Maximum mortgage maximum ceiling to own high-prices portion was $1,149,825, that’s 150% of the national compliant mortgage restrict. The latest FHA changes Illinois personal loans pass financial constraints getting Alaska, Their state, Guam plus the You.S. Virgin Islands to help you make up highest construction will set you back.

While looking taking right out a mortgage, you are able to an internet opportunities examine the choices. See Reputable to compare numerous lenders at the same time and choose the brand new you to into best option for you.

Down payments on a record highest

Higher loan limitations assist consumers accessibility large mortgage brokers but don’t assistance with off money. Large financial costs features pressed people to consider huge down costs as they consider hedge higher month-to-month mortgage loan money, according to a real estate agent statement.

Off payments rose by the fourteen.7% in the third one-fourth out of 2023 therefore the average down-payment number was $31,000. The typical down-payment due to the fact a buck number increased in every however, eleven states. Washington D.C., followed by Alaska, Montana, Connecticut and you can Rhode Isle, noticed the most big down-payment growth in 2023. Down money once the a share away from purchase price decrease from inside the five states: Idaho, Washington, Colorado and you can Utah.

“Increased home loan rates have increased the cost of resource a normal listed house with an effective 20% downpayment because of the more than $166 (otherwise seven.4%) when compared to last year,” Xu said. “In order to maintain a similar payment per month as one year in the past, a purchaser would have to enhance the down-payment so you’re able to 25.5%, requiring an upfront percentage greater than $23,300.”

If you are searching to reduce your house buying will cost you, it may help you evaluate your options to get the top mortgage price. Credible makes it possible to easily evaluate rates of interest off multiple loan providers in minutes.