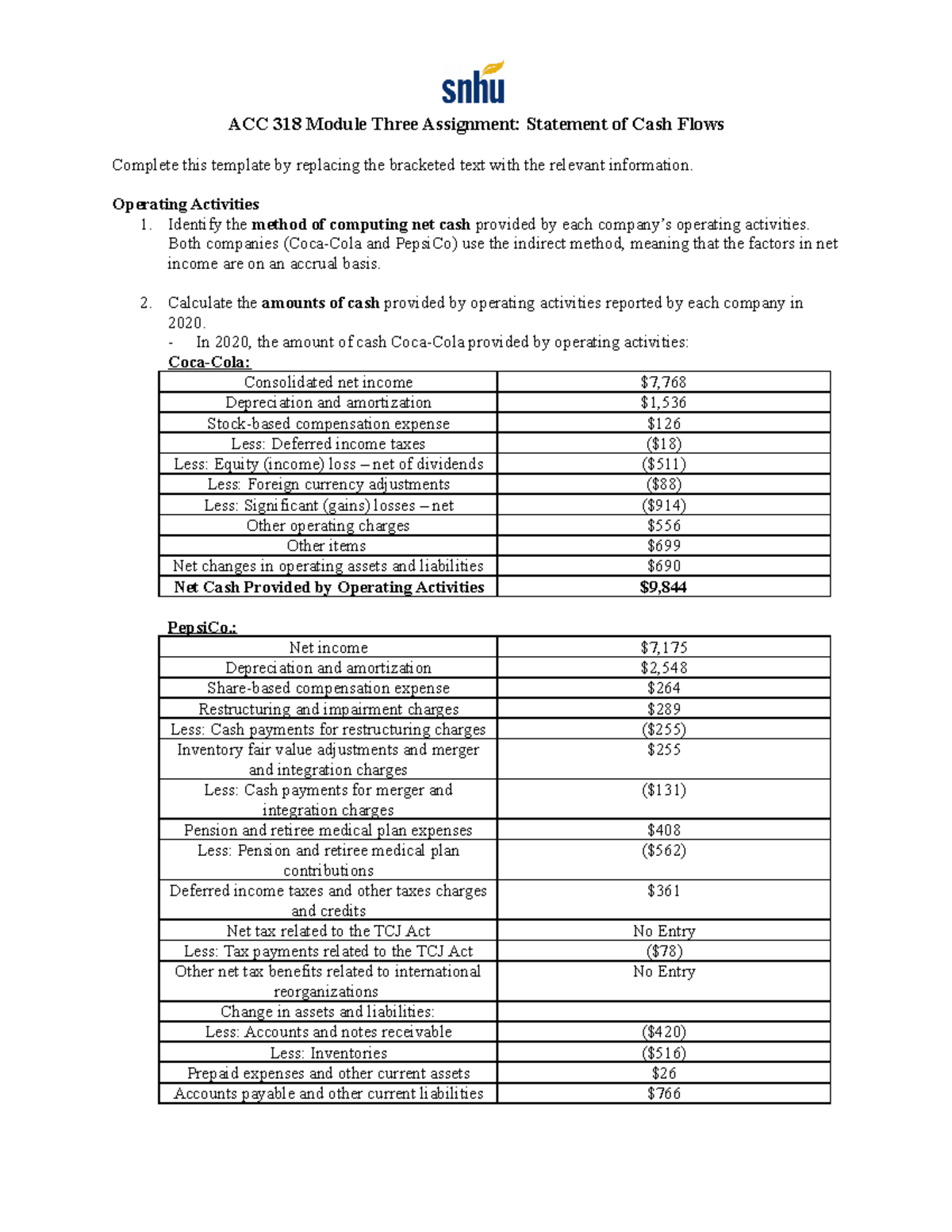

Today we are going to talk about the domestic guarantee loan, that’s easily become very popular having mortgage costs thus much higher.

Given that a typical 29-year repaired try closer to six%, these residents should not refinance and you may dump one to rates in the the process.

However if it nonetheless have to availableness the worthwhile (and you may abundant) house equity, they are able to take action via the next home loan.

One or two prominent choices are the house equity line of credit (HELOC) while the home guarantee loan, the latter from which enjoys a fixed interest while the capacity to take-out a lump sum payment of money from the home.

What is actually a house Equity Mortgage?

That money are able to be used to pay for some thing particularly as home improvements, to pay off other highest-interest fund, finance a down-payment for another house get, pay money for college tuition, and more.

Ultimately, you need the newest continues to own all you wish to. The house security loan just makes you tap into your accumulated home security without offering the underlying property.

Without a doubt, including a primary financial, you need to repay the mortgage through monthly premiums up until it try paid in full, refinanced, or perhaps the possessions marketed.

The application form procedure is comparable, in that you must provide earnings, a position, and you can house documentation, however it is usually less and less documents intensive.

Family Security Mortgage Example

This permits the latest borrower to get into extra loans while keeping this new good terms of the first-mortgage (and continue to pay it off into schedule).

Think a homeowner owns property respected within $650,000 and also a current mortgage which have an excellent equilibrium regarding $450,000 profitable site. Their attention price try 3.25% on a 30-year repaired.

Very house collateral loan lenders tend to restriction how much you could use in order to 80% or 90% of your house’s well worth.

Incase the mortgage name are two decades and the rate of interest try six.75%, you’d provides a payment away from $.

You would make this commission each month close to your first financial commission, however, carry out actually have an extra $70,000 on your own bank account.

As soon as we are the first-mortgage payment of $step one, we become a complete month-to-month regarding $2,, better lower than a prospective cash out refinance month-to-month out-of $step 3,.

Given that existing first mortgage possess instance a reduced speed, it’s wise to start an additional mortgage with a somewhat high rate.

Carry out Family Collateral Money Provides Fixed Prices?

A real household security mortgage will be feature a fixed interest. Put differently, the pace must not transform for your financing term.

Which differs from an excellent HELOC, which features a varying interest one to changes as soon as the perfect rates movements upwards otherwise down.

This basically means, HELOC interest levels was lower than similar household equity loan interest rates while they can get to switch higher.

Your efficiently shell out a made for a secured-for the rate of interest on the a home collateral loan. How much cash higher depends on the lender at issue plus personal loan functions.

House Collateral Loan Cost

The same as mortgage pricing, house collateral loan cost can and will will vary by the financial. So it’s important to shop around because you do a primary home loan.

In addition, costs would be firmly influenced from the features of the loan. Such as, a top shared loan-to-worthy of (CLTV) combined with a lowered credit rating commonly equate to a top rates.

On the other hand, a borrower with advanced borrowing from the bank (760+ FICO) whom simply borrows doing 80% otherwise a reduced amount of its home’s really worth can get be eligible for a significantly straight down rate.

Also keep in mind you to definitely interest levels was high toward next belongings and you can resource characteristics. And you can limitation CLTVs will likely be lower also.